Do You Know

How Much

Your Home is Worth?

Discover the Perfect Property with Expert Guidance

OUR NEIGHBORHOODS

Explore the neighborhoods we proudly serve across Brazoria, Fort Bend, and Matagorda counties. Whether you’re searching for top-rated schools, quiet country living, or quick access to Houston, our community pages will help you find your ideal home base.

Learn With Daphne: Real Estate Tips for Houston Suburbs

From homebuyer tips to neighborhood highlights, discover expert advice that makes your real estate journey easier and more inspiring.

Houston Suburbs

Under Contract! Now What? Escrow, Earnest Money & Title Commitment Explained

You're officially under contract on a home... now what? 🏡

In Part 1 of our "From Contract to Closing" series, Texas Real Estate Broker Daphne Brown breaks down exactly what happens behind the scenes from the moment your contract is executed to understanding your title commitment![cite: 1]

Whether you're buying or selling a home in Texas, knowing the rules around earnest money, option fees, firm deadlines (TREC Para. 5), and escrow will keep your transaction smooth and stress-free.[cite: 1]

👇 TIMESTAMPS / CHAPTERS 👇

00:00 - Introduction: Under Contract! Now What?

00:45 - What Does an Escrow Officer Actually Do?[cite: 1]

01:30 - Earnest Money vs. Option Fee (Crucial Differences)[cite: 1]

02:45 - The Option Period & TREC Paragraph 5 Deadlines[cite: 1]

04:10 - The 4 Stages of the Escrow Process (Contract to Keys)[cite: 1]

05:30 - How to Read Your Title Commitment (Schedules A, B, C & D)[cite: 1]

07:15 - Frequently Asked Questions (Earnest Money Refunds, Missed Deadlines & More)[cite: 1]

08:30 - What's Coming in Part 2![cite: 1]

💡 KEY TAKEAWAYS FROM THIS LESSON:

1. Escrow is a neutral third party that protects BOTH buyers and sellers.[cite: 1]

2. Earnest money & option fee deadlines are strictly enforced—time is of the essence![cite: 1]

3. Your Title Commitment (Schedules A–D) outlines who owns the property, exceptions, and liens that MUST be cleared before closing.[cite: 1]

📌 RELATED / NEXT VIDEO:

Catch Part 2 next week: Title Insurance Protections, Closing Delays, Surveys & Your Closing Day Checklist![cite: 1]

--------------------------------------------------

📲 CONNECT WITH DAPHNE BROWN:

Looking to buy, sell, or invest in Rosharon, Houston, or surrounding Texas markets? Let’s connect!

🏢 Beyond The Home Realty, LLC

📍 Servicing Rosharon, TX & Surrounding Areas

📞 Phone: [Insert Phone Number]

✉️ Email: [Insert Email Address]

🌐 Website: [Insert Website URL]

--------------------------------------------------

#TexasRealEstate #UnderContract #EarnestMoney #OptionPeriod #EscrowProcess #TitleCommitment #HomeBuyingProcess #HomeSellingTips #BeyondTheHomeRealty #DaphneBrown #RosharonTXRealEstate

Houston Suburbs

Houston Home Tour: 3911 Braden Dr N | 3 Bed, 2 Bath Near Medical Center & Pearland ($240K)

Welcome to 3911 Braden Drive North in Houston, TX! 🏠✨ Listed at $240,000, this move-in ready 3-bedroom, 2-bathroom home offers incredible location advantages, pristine upgrades, and zero back neighbors!

📍 LOCATION HIGHLIGHTS:

Sits practically next door to Tom Bass Regional Park and Adair Park, giving you instant access to walking trails, fishing lakes, playgrounds, and Clear Creek Golf Club. Plus, you’re just minutes from Hwy 288, Pearland, and the Texas Medical Center!

✨ PROPERTY FEATURES & UPGRADES:

• Great curb appeal with a mature shade tree, crisp new exterior paint, and a brand-new garage door.

• Fresh interior wood-look flooring and pristine walls with fresh paint.

• Spacious kitchen and dining combo featuring a brand-new range and hood vent.

• Sweet, private backyard space with no back neighbors—perfect for weekend relaxing.

• Fresh interior and exterior paint

• New garage door

• New ceiling fans

• New dishwasher

• New range and vent hood

📥 FREE REAL ESTATE RESOURCES & GUIDES:

🔹 Download My Free Home Buyer's Guide: https://daphnebrown.myflodesk.com/beforeyoubuy

🔹 Request A Free Home Valuation / Selling Strategy:

https://www.beyondthehomerealty.com

🗓️ SCHEDULE A PRIVATE SHOWING:

Ready to see this home in person or have questions about the Houston market?

👉 Book a consultation or request a showing: beyondthehomerealty.com

--------------------------------------------------

📲 CONNECT WITH DAPHNE BROWN & BEYOND THE HOME REALTY:

👤 Broker / Owner: Daphne Brown

🏢 Brokerage: Beyond The Home Realty, LLC

📞 Cell: 281-808-0471

📱 Office: 281-369-0909

✉️ Email: daphne@beyondthehomerealty.com

🌐 Website: https://www.beyondthehomerealty.com

📍 Serving: Houston, Pearland, Iowa Colony, Rosharon, Sealy, and surrounding Texas Suburbs

Follow on Socials:

📸 Instagram: @dbrownthetxrealtor

📘 Facebook: @dbrownthetxrealtor

--------------------------------------------------

⏰ CHAPTERS / TIMESTAMPS:

0:00 - Location & Tom Bass Regional Park

0:21 - Exterior & Curb Appeal

0:37 - Interior, Wood-Look Flooring & Fresh Paint

1:17 - Spacious Kitchen & Dining Combo

1:35 - Backyard & No Back Neighbors

1:46 - Pricing ($240,000), Location & How to Get More Info

--------------------------------------------------

#HoustonRealEstate #HoustonHomeTour #MoveInReadyHouston #TomBassPark #PearlandTX #TexasMedicalCenter #HoustonHomesForSale #BeyondTheHomeRealty #DaphneBrown #HoustonRealtor #FirstTimeHomeBuyer

Houston Suburbs

What Full-Service Real Estate Looks Like: How to Buy & Sell a House at the Same Time

Wondering how to buy and sell a house at the same time without double mortgages or temporary housing? 🏠✨ In this video, I take you inside a Beazer Homes inventory walkthrough in the Ellwood community (Iowa Colony, TX) while breaking down the exact strategy to buy and sell simultaneously.

As a real estate broker, my job is to offer full-service representation—monitoring new construction progress, negotiating timeline contingencies, and aligning your closing dates so your move is completely seamless. Whether you're looking at Beazer Homes in Ellwood or managing a home sale while building, here is what full-service guidance looks like.

📥 ACCESS OUR FREE REAL ESTATE RESOURCES & GUIDES:

Fill out one quick form and I'll send these your way over the next several days:

🔹 The New Construction Guide

🔹 The New Construction Insider's Guide

🔹 The Ultimate Home Buyer's Workbook

👉 Get started here: https://daphnebrown.myflodesk.com/newhomeconstruction

🔹 Request The FREE Buying and Selling Simultaneously Guide HERE!

https://daphnebrown.myflodesk.com/b2nbafzx7v

🗓️ SCHEDULE A FREE CONSULTATION:

Ready to buy, sell, or build your dream home? Let's map out your strategy!

Book your session here: https://www.beyondthehomerealty.com

📲 CONNECT WITH DAPHNE BROWN & BEYOND THE HOME REALTY:

👤 Broker / Owner: Daphne Brown

🏢 Brokerage: Beyond The Home Realty, LLC

📞 Cell: 281-808-0471

📱 Office: 281-369-0909

✉️ Email: daphne@beyondthehomerealty.com

🌐 Website: https://www.beyondthehomerealty.com

📍 Serving: Houston, Iowa Colony, Rosharon, Pearland, Sealy, and surrounding Texas Suburbs

Follow me on Socials:

📸 Instagram: @dbrownthetxrealtor

📘 Facebook: @dbrownthetxrealtor

--------------------------------------------------

⏰ CHAPTERS / TIMESTAMPS:

0:00 - Introduction: What Full-Service Real Estate Means

1:17 - How to Buy and Sell a House at the Same Time

1:55- Inventory Home Walkthrough- The Lynwood Floorplan

6:35- Did I really just do that?

7:50- More at Ellwood

8:08- What I Need From You

8:22 - Free Home Buying & Selling Resources

8:58 - Let's Work Together

--------------------------------------------------

#BuyingAndSellingAtTheSameTime #BeazerHomes #EllwoodIowaColony #IowaColonyTX #HoustonRealEstate #NewConstructionTexas #BeyondTheHomeRealty #DaphneBrown #TexasRealtor #InventoryHomes

Houston Suburbs

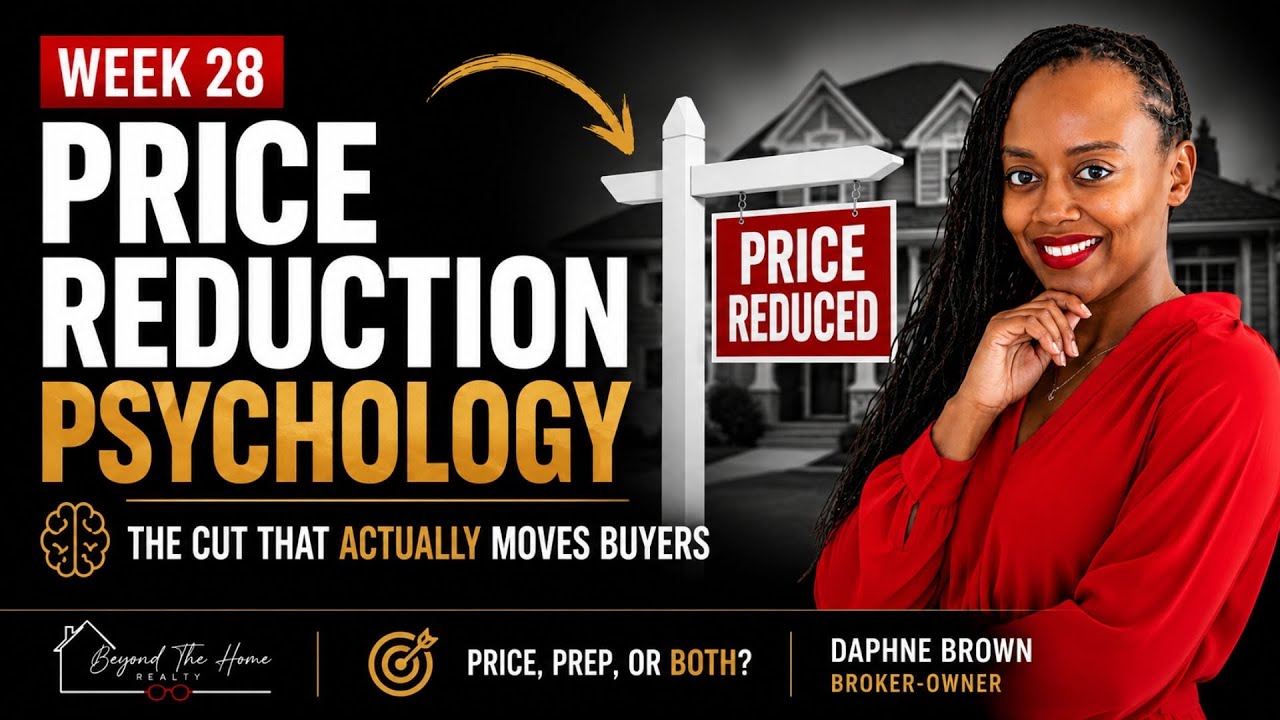

Why Your House Isn't Selling: Price, Prep, or Both? #Texashomeseller #texashomes #texas

Struggling with a house that’s sitting on the market? When your listing goes stale, the biggest question is always: is it a price problem, a marketing problem, or both?

In this video, we dive deep into the real estate market "Adjustment Playbook" to show you exactly how to read showing feedback, when to lower your home price, and the precise psychology behind a successful price reduction that actually moves buyers.

We’ll bust common real estate myths—like whether canceling and relisting truly resets cumulative days on market (DOM)—and walk through a real-life case study of a home that went from 0 offers to sold in 30 days by pairing professional photography with a single, confident strategic price move.

Whether you are a listing agent trying to advise your sellers or a homeowner wondering why your home isn't selling, this strategy guide will give you a clear action plan.

👇 Grab your checklist and let's connect:

🏠 Website: https://BeyondTheHomeRealty.com

📧 Email: daphne@BeyondTheHomeRealty.com

📞 Let's Talk: 281-808-0471

CHAPTERS:

0:00 - Why Your House Isn't Selling (The 2-Week Rule)

01:45 - The Psychology of a Price Cut: Anchoring & Loss Aversion

04:10 - The Left-Digit Effect & Pricing Thresholds

06:20 - Small, Scattered Cuts vs. One Confident Move

08:05 - Weak Photos vs. Price: Which Lever Is Broken?

10:40 - The "Both" Decision: Relaunching Prep and Price Together

12:55 - Does Relisting Reset Days on Market? (The MLS Truth)

15:45 - Real Estate Case Study: From Stale Listing to Sold in 30 Days

18:15 - Your Step-by-Step Adjustment Playbook Checklist

About Daphne Brown-Woodard:

Daphne Brown-Woodard is a professional Real Estate Broker-Owner of Beyond The Home Realty, LLC, based in Texas. Serving Rosharon, Brazoria County, and the Houston suburbs, Daphne is an ABR®, e-PRO®, and RENE certified REALTOR® dedicated to consumer advocacy and strategic marketing that gets properties sold.

#RealEstatePricing #HomeSellingTips #PriceReductionStrategy #TexasRealEstate #BeyondTheHomeRealty #ListingAgent #SellingAHome

Your Next Move, Simplified

Whether you’re buying your first home or preparing to sell, we’ve created resources to help you every step of the way.

Buyer’s Guide

A step-by-step overview of the home buying process, designed to help you feel informed, prepared, and confident from your first showing to closing day.

Thinking of Selling?

Smart strategies and expert insights to help you prepare your home, price it effectively, and navigate the selling process with clarity.

Before You Buy in 2026

A practical guide to preparing for homeownership, including financing basics, market timing, and smart planning steps to help you buy with confidence in the year ahead.

Before You List Guide

A seller-focused checklist covering preparation, pricing considerations, and presentation tips to help your home stand out and attract serious buyers.

What Credit Score Do You Actually Need to Buy a House?

Clear, straightforward insight into how credit impacts home buying, what lenders really look for, and steps you can take to strengthen your financial position.

New Construction Guide

An insider look at the new construction process, including timelines, builder incentives, upgrades, inspections, and what to know before signing a contract.

MEET

Daphne Brown-Woodard

Daphne Brown strives to exceed her clients' expectations and supply them with the necessary information to understand the entire home buying or selling process from beginning to the end. She is committed to listening to her clients' needs and utilizing her keen negotiation skills to ensure a successful transaction.

OUR STANDARD

DETAIL-DRIVEN PROCESS

Thoughtful preparation, intentional marketing, and strong advocacy

INTEGRITY-LED SERVICE

Advice rooted in transparency, care, and long-term relationships